All Categories

Featured

Table of Contents

No-load Multi-Year Assured Annuities (MYGAs) on the RetireOne system deal RIAs and their customers security versus losses with an assured, taken care of rate of return. These solutions are interest-rate sensitive, yet might offer insurance attributes, and tax-deferred growth. They are favored by conventional capitalists looking for rather foreseeable end results.

3 The Squander Choice is an optional feature that needs to be elected at agreement issue and based on Internal Earnings Code constraints. Not readily available for a Certified Longevity Annuity Agreement (QLAC). Your lifetime earnings settlements will be lower with this choice than they would certainly lack it. Not available in all states.

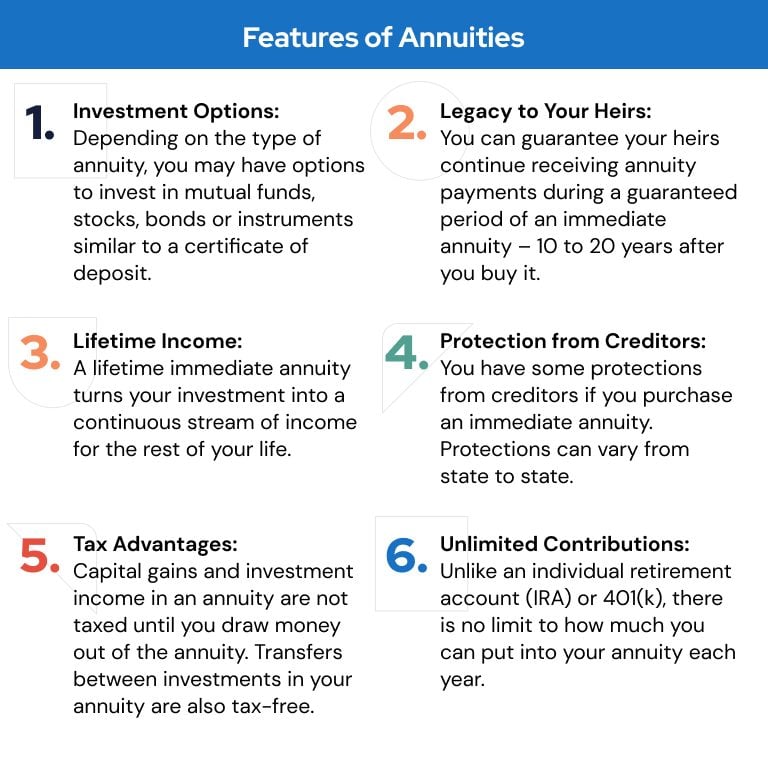

An annuity is an agreement in which an insurance provider makes a collection of revenue payments at routine periods in return for a premium or costs you have paid. Annuities are usually purchased for future retirement earnings. Just an annuity can pay a revenue that can be ensured to last as long as you live.

The Best Annuity Companies

One of the most typical sorts of annuities are: solitary or numerous costs, prompt or deferred, and taken care of or variable. For a single costs contract, you pay the insurer just one settlement, whereas you make a series of repayments for a numerous premium. With an immediate annuity, revenue payments begin no later on than one year after you pay the costs.

Usually, what these prices will be is totally up to the insurance provider. The existing rate is the rate the firm decides to credit rating to your agreement at a particular time. The company will ensure it will not alter prices for a specific amount of time. The minimum guaranteed interest price is the most affordable rate your annuity will gain (deferred income annuity quote).

Some annuity agreements apply various rate of interest rates per premium you pay or to costs you pay throughout different amount of time. Other annuity contracts might have two or more built up values that fund various benefit options. These collected worths may utilize various rates of interest. You get just one of the gathered values depending upon which profit you select.

Under existing federal legislation, annuities obtain unique tax treatment. Earnings tax on annuities is deferred, which indicates you are not exhausted on the rate of interest your money makes while it stays in the annuity.

Many states' tax laws on annuities adhere to the government law. Lots of states have laws that provide you a set number of days to look at the annuity contract after you acquire it.

The "totally free look" period need to be prominently stated in your agreement. Make sure to review your agreement carefully throughout the "totally free appearance" duration. You need to consider what your goals are for the cash you take into any annuity. You require to think of just how much danger you want to take with the cash as well.

Tax Deferred Annuity Withdrawal

Terms and conditions of each annuity agreement will differ. Ask the agent and business for an explanation of anything you do not understand. Do this prior to any type of complimentary look duration finishes. Compare details for comparable contracts from several companies. Comparing products might help you make a much better choice. If you have a details concern or can not obtain answers you require from the representative or firm, call the Division.

:max_bytes(150000):strip_icc()/annuity-ladder.asp-final-bb1e6602acd2498ead56e5f8bcb458c3.png)

There are two standard kinds of annuity contracts: instant and delayed. An instant annuity is an annuity contract in which settlements start within 12 months of the day of acquisition.

Regular repayments are postponed until a maturation date specified in the agreement or, if earlier, a date picked by the owner of the contract. what is the basic function of an annuity. The most typical Immediate Annuity Agreement settlement options consist of: Insurance firm makes routine payments for the annuitant's life time. An alternative based upon the annuitant's survival is called a life set alternative

There are two annuitants (called joint annuitants), generally spouses and regular settlements continue till the fatality of both. The revenue settlement quantity might proceed at 100% when just one annuitant lives or be decreased (50%, 66.67%, 75%) during the life of the making it through annuitant. Routine payments are produced a specified time period (e.g., 5, 10 or 20 years).

Annuity Vs Dividend

Some immediate annuities supply inflation security with routine boosts based upon a fixed price (3%) or an index such as the Customer Price Index (CPI). An annuity with a CPI adjustment will start with lower settlements or need a greater preliminary premium, yet it will certainly give at least partial security from the danger of rising cost of living.

Earnings payments continue to be constant if the financial investment efficiency (after all charges) amounts to the assumed financial investment return (AIR) specified in the contract. Immediate annuities generally do not allow partial withdrawals or supply for cash money surrender advantages.

Such individuals should look for insurance providers that use low quality underwriting and think about the annuitant's wellness status in identifying annuity income settlements. Do you have sufficient monetary resources to fulfill your income needs without purchasing an annuity?

5 Year Deferral Inherited Annuity

For some alternatives, your wellness and marital condition may be considered (annuity account information). A straight life annuity will certainly offer a higher regular monthly income payment for a given costs than life contingent annuity with a period specific or refund feature. To put it simply, the expense of a specified revenue repayment (e.g., $100 per month) will be greater for a life contingent annuity with a duration specific or refund function than for a straight life annuity

For example, an individual with a reliant partner may intend to take into consideration a joint and survivor annuity. A person worried about getting a minimal return on his/her annuity costs may desire to take into consideration a life contingent alternative with a duration specific or a refund feature. A variable immediate annuity is frequently chosen to maintain rate with rising cost of living during your retirement years.

A paid-up deferred annuity, also frequently referred to as a deferred income annuity (DIA), is an annuity contract in which each costs repayment acquisitions a fixed dollar revenue benefit that commences on a specified day, such as an individual's retired life day. how much can you put in an annuity. The contracts do not preserve an account value. The premium cost for this item is much less than for a prompt annuity and it allows a person to maintain control over many of his/her various other assets throughout retirement, while safeguarding longevity security

Each premium settlement purchased a stream of earnings. At an employee's retired life, the income streams were combined. purchasing annuities. The company might make best use of the employee's retired life advantage if the contract did not offer for a fatality benefit or cash money abandonment benefit. Today, insurers are marketing a similar item, frequently described as durability insurance policy.

A lot of contracts allow withdrawals below a defined degree (e.g., 10% of the account worth) on an annual basis without surrender fee. Buildup annuities usually give for a cash settlement in the event of fatality prior to annuitization.

{kind=link}

Table of Contents

Latest Posts

Understanding Financial Strategies Everything You Need to Know About Financial Strategies Defining the Right Financial Strategy Pros and Cons of Fixed Income Annuity Vs Variable Growth Annuity Why Fix

Highlighting What Is Variable Annuity Vs Fixed Annuity Everything You Need to Know About Fixed Interest Annuity Vs Variable Investment Annuity Defining the Right Financial Strategy Features of Smart I

Breaking Down Fixed Annuity Or Variable Annuity Everything You Need to Know About Financial Strategies Breaking Down the Basics of Variable Annuity Vs Fixed Indexed Annuity Advantages and Disadvantage

More

Latest Posts